Umbrella Insurance in Tennessee: How Much Coverage Do You Need?

Umbrella insurance in Tennessee can be one of the simplest ways to protect your family from a large liability claim. If you live in Franklin, Brentwood, or anywhere across Williamson County, your home, vehicles, lake property, teen drivers, and lifestyle may create more exposure than a standard policy can handle. At Holt Insurance, we help families look at the full picture so coverage feels clear, not complicated.

The Problem: Standard Liability Limits May Not Be Enough

Most home and auto policies include liability coverage.

That is the part of your policy that can help pay if you are legally responsible for injuring someone or damaging their property.

But liability claims can get expensive quickly.

For example:

A serious auto accident involving multiple people

A guest injured at your pool

A boating accident on Center Hill Lake or Tims Ford Lake

A teen driver causing a major crash

A lawsuit after an accident at your home

A dog bite or ATV injury

Tennessee’s minimum auto liability requirements are much lower than what many affluent families would want protecting them. The Tennessee Department of Revenue lists minimum auto liability limits at $25,000 per injury or death, $50,000 total per accident, and $25,000 for property damage.

For a family with a $1.5M home, multiple vehicles, and meaningful assets, those numbers can leave a lot exposed.

What Is Personal Umbrella Insurance?

Personal umbrella insurance is extra liability coverage that sits above your home, auto, boat, or other eligible policies.

Simple definition:

Umbrella insurance helps protect you when a liability claim is larger than the limits on your underlying policy.

For example, if your auto policy has $500,000 of liability coverage and a covered claim reaches $1.2M, an umbrella policy may help cover the amount above your auto limit, up to the umbrella policy limit.

The Insurance Information Institute notes that many insurers require higher underlying limits, often around $250,000 on auto liability and $300,000 on homeowners liability, before offering an umbrella policy.

Who Needs Umbrella Insurance in Tennessee?

Umbrella insurance is worth reviewing if your family has:

Teen drivers

A lake house or second home

Boats, jet skis, ATVs, or golf carts

A pool or trampoline

Dogs

Rental property

Significant savings, investments, or future income

Frequent guests, parties, or hosted events

For many Holt clients, the question is not, “Do we need umbrella coverage?”

The better question is, “How much umbrella coverage fits our life?”

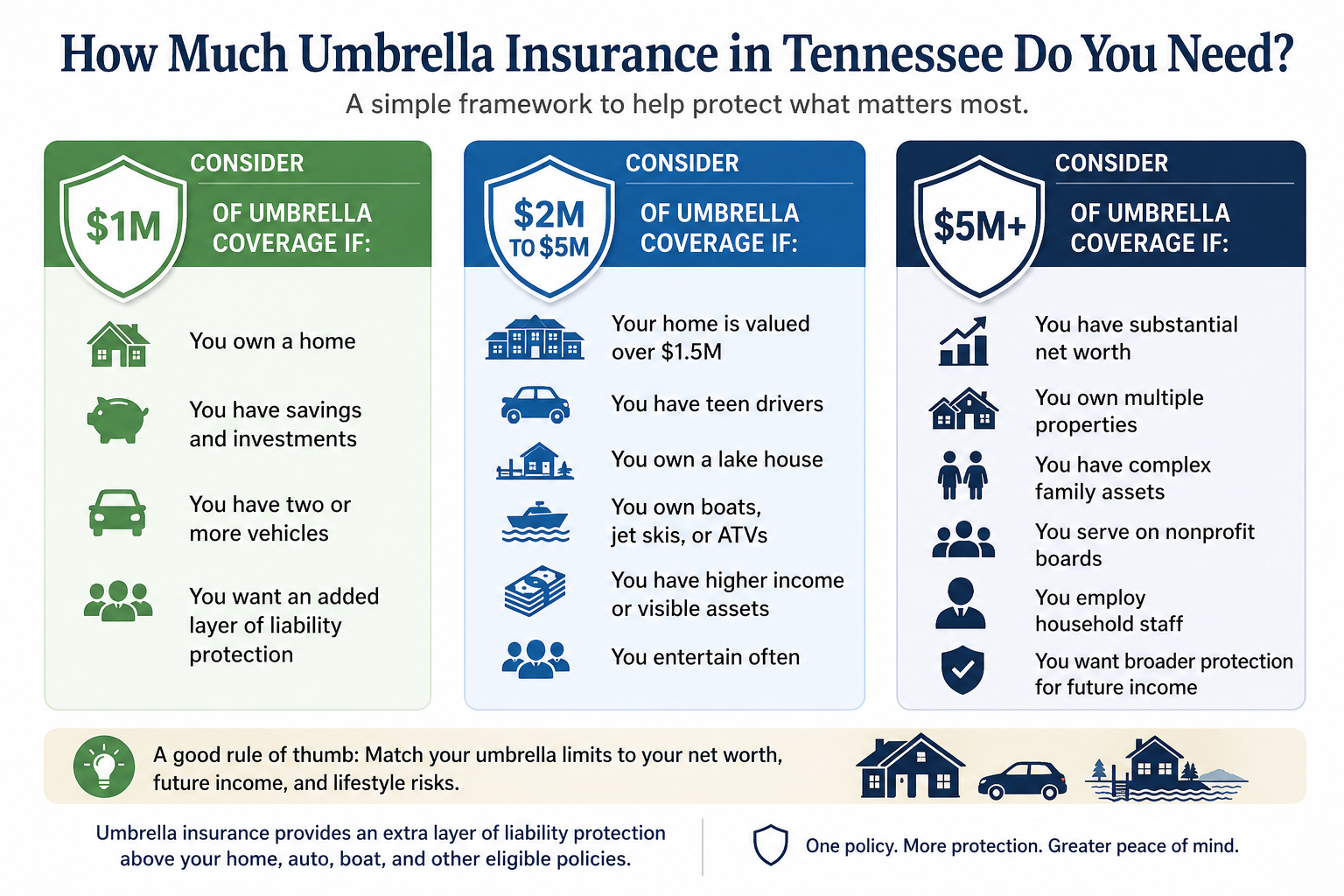

How Much Umbrella Insurance in Tennessee Do You Need?

A common starting point is $1M.

But many affluent Tennessee families should consider $2M, $5M, or more depending on their assets and risk.

Here is a simple framework.

Consider $1M if: You own a home, have savings and investments to protect, own two or more vehicles and you want an added layer of liability protection.

Consider $2M to $5M if: Your home is valued over $1.5M, have teen drivers, own a lake house, own boats, jet skis, or ATVs, have higher income or visible assets and you entertain often.

Consider $5M or more if: You have substantial net worth, own multiple properties, have complex family assets, serve on nonprofit boards, employ household staff and want broader protection for future income.

A good rule of thumb is to review umbrella limits against your net worth, future income, and lifestyle risks. Kiplinger notes that umbrella policies are commonly sold in $1M increments and that coverage needs often depend on both assets and lawsuit risk

What Does Umbrella Insurance Usually Cover?

Umbrella coverage may help with:

Bodily injury liability

Property damage liability

Legal defense costs

Certain personal injury claims, such as libel or slander

Claims involving covered auto, home, boat, or recreational exposures

Coverage varies by policy and carrier, so the details matter.

That is why it helps to review umbrella insurance with someone who understands your full household, not just one policy at a time.

What Umbrella Insurance Usually Does Not Cover

Umbrella insurance is broad, but it does not cover everything.

It typically does not cover:

Damage to your own property

Your own injuries

Intentional harm

Business liability unless specifically included

Certain excluded vehicles or recreational equipment

Claims outside policy terms

This is why your underlying policies need to be coordinated properly.

An umbrella policy is not a substitute for strong home, auto, boat, or recreational vehicle coverage. It is an added layer.

Why Tennessee Families Should Review Umbrella Coverage Regularly

Your liability exposure changes over time.

You may need more coverage after:

Buying a larger home

Adding a teen driver

Purchasing a lake house

Buying a boat, ATV, or golf cart

Renovating a home

Hosting more events

Growing your savings or investments

Adding rental property

Joining a board or community organization

In Middle Tennessee, life can change quickly. One year you are adding a vehicle for a new driver. The next year you are buying a lake place or upgrading your home.

Your insurance should keep up.

Why Work With Holt Insurance?

At Holt Insurance, we believe in People, Not Policies. That means we do not just ask, “What limit do you want?” We ask better questions:

Our family has served Tennessee families since 1946. We help simplify complex coverage so you can focus on what matters.

If you want a clear, personalized review of your liability coverage, reach out to Holt Insurance today. We can help you decide whether umbrella insurance makes sense and how much coverage may fit your family.

Frequently Asked Questions

-

Umbrella insurance is extra liability coverage that can help protect you after your home, auto, or other underlying liability limits are used up.

-

Many families start with $1M, but higher net worth families often consider $2M, $5M, or more. The right amount depends on your assets, income, vehicles, properties, and lifestyle risks.

-

You still may. High home and auto limits are important, but a serious claim can exceed them. Umbrella coverage adds another layer of protection.

-

Yes. Teen drivers can increase liability exposure, especially in households with multiple vehicles or higher-value assets.

-

It may, but only if the underlying policies and umbrella policy are written correctly. Boats, jet skis, and secondary homes should be reviewed carefully.

-

It is often more affordable than people expect, especially compared to the amount of protection it can provide. Pricing depends on your household, vehicles, properties, drivers, and coverage limits.