Classic Car Insurance in Tennessee: Agreed Value vs Actual Cash Value

If you own a classic car in Tennessee, whether it is a restored Mustang in Franklin or a vintage truck you take to weekend shows around Brentwood, your insurance matters more than most people realize. The biggest question we see is this, should your policy be agreed value or actual cash value? The difference can mean thousands at claim time. Let’s walk through it in plain English so you can protect what you have built.

What Makes Classic Car Insurance Different?

Classic cars are not like daily drivers.

They are:

Appreciating or stable in value, not depreciating

Often restored or customized

Driven less frequently

Stored more carefully

Because of that, standard auto insurance often falls short.

That is where classic car insurance in Tennessee comes in. It is designed for collector vehicles and gives you more control over how your car is valued.

The Core Problem Most Owners Miss

Most policies default to actual cash value, and that can create a gap.

Here is the issue:

You may have invested $75,000 into a restoration

The insurance company may value it at $35,000 based on age and depreciation

In a total loss, that is all you receive

For affluent families with collections, multiple vehicles, or rare models, this is a real risk.

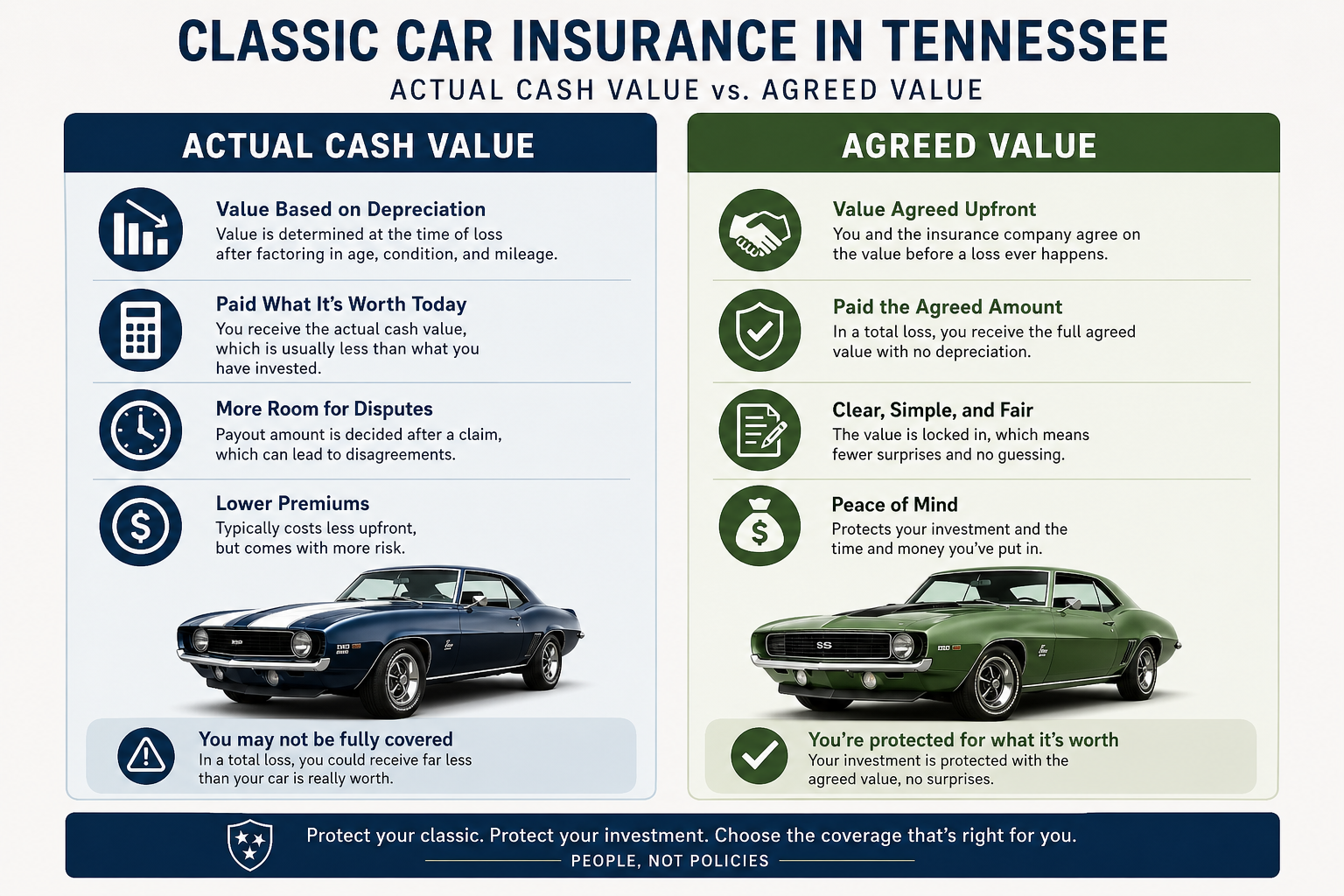

What Is Actual Cash Value?

Actual Cash Value (ACV) means:

The value of your car today after depreciation.

In simple terms:

The insurer looks at age, condition, mileage

Then subtracts depreciation

You are paid what they believe it is worth today

Why This Can Be a Problem

For classic cars:

Depreciation does not apply the same way

Market value can actually increase

Custom upgrades are often undervalued

Tennessee Example

A Brentwood client owns a restored 1969 Camaro:

Restoration cost: $90,000

Market comps: $85,000 to $110,000

ACV payout estimate: closer to $50,000 to $60,000

That gap is where frustration happens.

What Is Agreed Value?

Agreed Value means:

You and the insurance company agree upfront on what the car is worth.

That number is written into the policy.

If there is a total loss:

You receive the agreed amount

No depreciation

No arguing at claim time

Why Affluent Owners Prefer This

Agreed value provides:

Certainty

Protection for restoration investment

Alignment with collector market values

Side-by-Side Comparison

Actual Cash Value

Based on depreciation

Value determined at claim time

Lower premiums, but higher risk

Often used in standard auto policies

Agreed Value

Value set upfront, no depreciation

Higher confidence in claims

Designed for collector and classic vehicles

Who Needs Agreed Value Coverage?

If you fall into any of these categories, it is worth a closer look:

You own a classic or antique vehicle

Your car has been restored or customized

You attend shows or collector events

You keep vehicles at a second home or lake property

You have multiple specialty vehicles

Many families in Williamson County and across Middle Tennessee fall into this group.

How Value Is Determined

For agreed value policies, insurers typically look at:

Professional appraisals

Photos and documentation

Restoration records

Market comparisons

This ensures the number is fair and defendable.

Common Mistakes to Avoid

Even high-net-worth families make these:

Assuming their standard auto policy covers full value

Not updating value after restoration

Forgetting about vehicles stored at secondary homes

Not bundling coverage with a single advisor

Insurance works best when it is coordinated, not pieced together.

How This Fits Into Your Bigger Insurance Picture

Classic cars are just one piece. That is where working with a relationship-driven agency matters.

If you want a clear, personalized review of your classic car coverage, reach out to Holt Insurance today.

Our family has been serving Tennessee families since 1946, and we are here to help you protect what matters, without confusion or guesswork.

Frequently Asked Questions

-

Yes, typically a bit more. But you are paying for certainty. For most classic car owners, the added protection is worth it.

-

In many cases, yes. Insurers want documentation to support the value. This helps avoid disputes later.

-

Absolutely. If you restore or the market changes, your policy should be reviewed and adjusted.

-

Yes. Many policies assume limited use, like weekend driving or shows. Lower mileage can help keep premiums reasonable.

-

They can be, but it needs to be structured correctly. Storage location and usage both matter.

-

You will likely be covered at actual cash value, which may leave a significant gap if there is a loss.